The LancetGate refers to a controversy surrounding Gilead Sciences, the pharmaceutical company developing Remdesivir. Gilead has a complex history, initially founded as Oligogen in 1987.

In 2011, the company shifted its focus to hepatitis C with the acquisition of Pharmasset for $11 billion, leading to a pricing controversy over the drug Sovaldi in 2014. Gilead faced criticism for the high cost of the medication, reaching around 40,000 euros, and subsequent disputes over its patent in 2018.

Gilead expanded its portfolio with the acquisition of KitePharma in 2017 for $11.9 billion, specializing in oncology. Additionally, a partnership with Belgian biotech company Galapagos was established in 2015, and Gilead increased its stake in Galapagos to 22% in 2019, investing $5 billion.

In March 2020, Gilead announced the acquisition of Forty Seven, a specialist in blood cancers, for $4.9 billion. The LancetGate controversy raises questions about Gilead's role in the development and promotion of Remdesivir amid concerns and debates surrounding its various acquisitions, pricing practices, and patent disputes.

A partnership with a Belgian biotech company Galapagos was signed in 2015. KitePharma, a specialist in oncology, was acquired in 2017 for $11.9 billion. Then in 2019, Gilead increased its stake in Galapagos from 12.3% to 22% of the capital by investing $5 billion, with the objective of establishing a global R&D collaboration. Finally in March 2020, Gilead announced the acquisition of Forty Seven, a blood cancer specialist for $4.9 billion.

Ses Activités de Lobbying

In 2018, Gilead reportedly allocated $2.9 million for lobbying activities in the United States, a figure that escalated to $5,720 million in 2019. The first quarter of 2020 alone accounted for $2.45 million, constituting 43% of the 2019 total and 82% of the 2018 total. These extensive lobbying expenditures underscore Gilead's proactive engagement in influencing policy and decision-making processes.

In comparison to other industries, the pharmaceutical sector, to which Gilead belongs, holds a substantial position in lobbying, representing 8.5% of the total expenditure in the United States.

This places it ahead of the electronics and insurance industries, which account for 4.5% and 4.4%, respectively. The detailed article provides an insightful overview of Gilead's lobbying strategies and financial allocations in shaping legislative and regulatory landscapes.

In 2018 Gilead would have spent $2.9 million on lobbying in the USA alone and declared $5,720 million for 2019. For the first quarter of 2020 alone, the activities reported to the American Center for Responsive Politics (CRP) are 2 .45 million dollars , or 43% of the sums of 2019 and 82% of 2018. A detailed article summarizes the company's lobbying expenses

En Conclusion

The detailed accounts annex highlights significant risks and concerns associated with the pharmaceutical company in question. These include fears of reimbursement ceilings for patented drugs, the emergence of generics, legal risks related to patent infringement, and the risk of R&D failure despite substantial investments.

The company's strong financial position is noted, but vulnerabilities are pointed out, such as over-reliance on a single pathology (HIV), limited R&D project success, and a strategy of repurchasing its own shares.

The lack of transparency regarding lobbying expenses and the company's registration in a low corporate tax jurisdiction raise ethical questions.

The connection between Gilead and The Lancet, along with suspicions of market manipulation and potential conflicts of interest, suggests a need for investigation.

The ongoing debate around the inclusion of Remdesivir in medical trials raises concerns about the credibility of scientific studies and calls for scrutiny into decision-making processes by health authorities.

Gilead's share price fluctuates according to announcements with strange coincidences. This leads to suspicions of stock price manipulation ( Reuters June 1, 2020 )

The commission of inquiry will have a heavy job updating this story . Above all, it will have to ask itself the question of how did we manage to include Remdesivir in the Discovery test with a very low level of real evidence of its effectiveness? And how was the High Committee for Public Health able to include Remdevisir in its recommendations?

The discrediting of hydroxychloroquine through a study on a very large sample size, published in a prestigious and respected journal, leaves room for doubt.

Et en Annexe

The financial analysis of Gilead's 2019 accounts reveals several key points.

The company heavily relies on HIV treatments, constituting 78% of its revenue, posing a vulnerability to generic alternatives. Research and development (R&D) projects include anti-inflammatory and anti-fibrosis treatments, showing a need for diversification.

Risks involve potential significant damages and royalty payments due to ongoing litigations. Noteworthy is the significant share buyback program, raising questions about the company's transformation into a financial holding.

The detailed cash flow analysis indicates substantial financial activities beyond R&D, resembling a financial investment approach. Despite high R&D spending, the decline in 2019 revenue raises concerns about the effectiveness of these investments. The company's focus on external growth and franchising distribution strategy may contribute to revenue concentration risks.

Overall, Gilead's financial position, with a net result of $5.386 billion, appears stable but faces challenges related to revenue concentration and uncertainties in R&D effectiveness.

ANNEX

The devil is in the detail, we have provided the elements of analysis for those who may be interested.

1. Synthetic financial analysis of Gilead's 2019 accounts ($ billion should be interpreted as billions of dollars)

The financial analysis of a pharmaceutical company must focus on the following points: Turnover and concentration of this turnover, R&D expenditure and progress of the various treatments according to the various phases of clinical testing, possible risks. In the case of Gilead, what we can mainly note:

A high concentration of turnover : 78% is made on treatments against HIV leading to dependence on one or two treatments. The report offers a very detailed analysis of the points of vulnerability with regard to emerging generic treatments, combined with an almost obsessive priority of maintaining profitability.

On research and development (R&D): among their project being studied in phase 3: a pulmonary anti-inflammatory and an anti-pulmonary fibrosis product, which would correspond to the need for diversification, nothing surprising given the current context. In addition, nine pages on ecological investments and actions which would aim to seduce environmentalists and clear their conscience, because it is difficult to interpret their purpose. It should seem obvious that medical R&D is carried out in an “ethical, responsible and environmentally friendly” manner.

On risks: page 15: “We may be required to pay significant damages and royalty payments as a result of ongoing litigation involving Yescarta and Biktarvy. If the jury's verdict is not upheld on appeal, the loss will be void. If the jury verdict is upheld in its entirety on appeal, we estimate that the upper end of the range of possible losses through December 31, 2019 is approximately $1.6 billion ."

No information mentions lobbying expenses by geographic area. Apart from what we could find in the CRP above. This therefore makes a possible audit on lobbying delicate since it is not specified in the accounts.

Finally, a significant element, the repurchases of its own shares for 9 billion dollars over 3 years. Self-ownership has reached such a level that we can ask ourselves the question of this action which is generally a method used to counter hostile attempts at a public purchase offer. However, at such a level, we can ask ourselves the question if the company is not transforming into a financial holding company for which there is an interest in causing upward speculation effects. For example, a positive announcement effect on a treatment leads to an increase in the company's stock: if the price rises, the company reduces the shares it owns and collects the initial price more surplus value, conversely, loses .

2. Accounts in detail

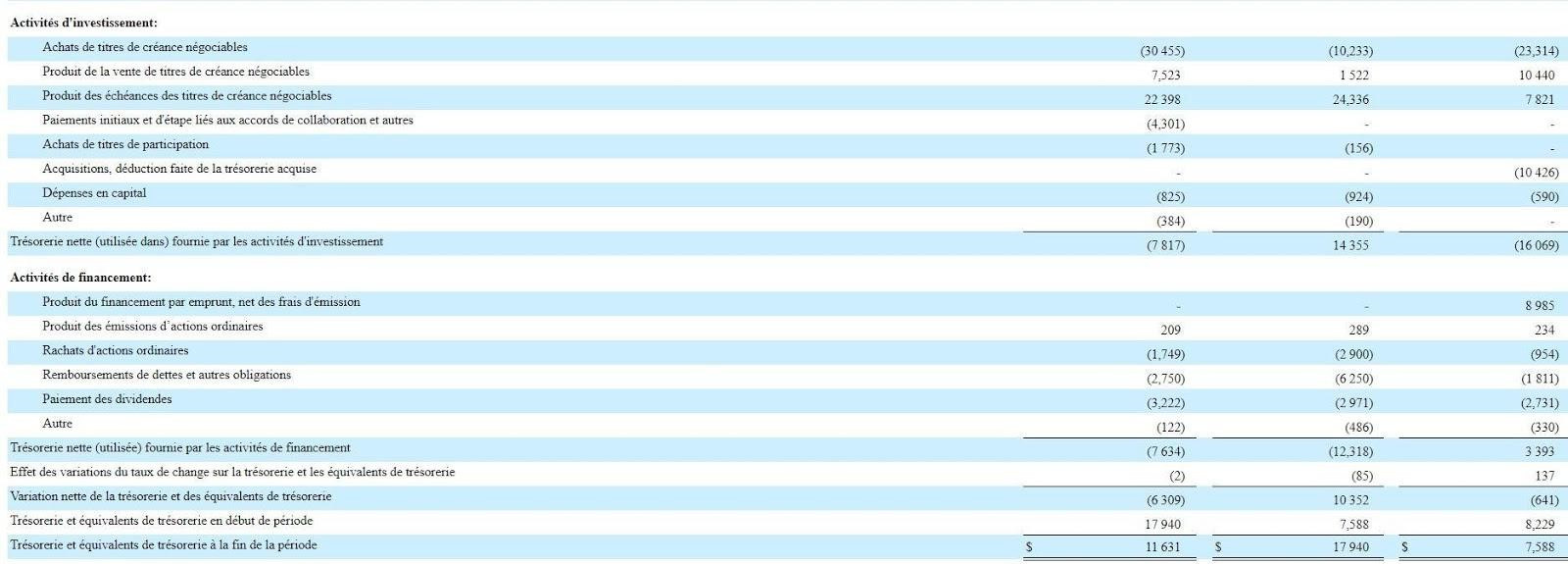

The cash flow statement

The consolidated cash flows (overall Cash Flow of a group) are made up of 3 sub-groups:

The operating cash flow which corresponds to the remaining balance, after having deducted only operating expenses from operating income (turnover and other miscellaneous operating income).

The investment cash flow which corresponds to the remaining balance after having deducted from the disposals of fixed assets (investment products) only the investment expenses (investment charge).

The financing cash flow which corresponds to the remaining balance after deducting the raising of new funds (equity, new borrowings) disposals of fixed assets (investment products) only financing expenses (financing charges, including borrowings reimbursed, including dividends paid for $3.2 billion, including share buybacks for $1.759 billion ).

Details and clarifications on the cash flow variation table.

R&D expenses: $9.1 billion recognized as operating expenses.

Operating cash flow: $ 9.1 billion (difference between turnover and operating expenses, but before financial expenses, exceptional expenses or income and before corporate tax).

Investment cash flow: -$7.8 billion (difference between investment expenditure on the purchase of negotiable debt securities expected to provide returns, shares, including its own, and resales of securities and shares of the same type ).

GILEAD certainly does R&D, but its financial activities (sale and purchase of securities) reach very significant levels with between $20 and $30 billion in purchases/resales of negotiable securities each year. Would it have become more of an investment fund type financial holding company than a pharmaceutical laboratory finding new marketable products?

Financing cash flow: -$7.6 billion after $3.2 billion in dividend payments (difference between what comes in and what goes out for pure financial operations: differential between dividends received and dividends paid, capital repayment of the debt previously raised).

Reformulation of the result by reasoning only on operations “excluding financial operations, but retaining the dividends paid”. This is what the accounts of the Gilead company could give.

Operating cash flow : $9.1 billion

Less the bank debts repaid in capital : $2.8 billion (note: the cash flow allows this to be paid because the capital to be repaid is not an operating expense, therefore does not reduce the calculated Cash Flow. Once the debt is repaid there remains what is called Free Cash Flow: what remains net in the coffers once everything has been paid).

Free cash flow at this stage: approximately $5 billion ( $9.1 billion – $2.8 billion – financial costs of $1 billion at this stage and exceptional income/expenses).

Repurchase of its own shares: $1.7 billion (legal treasury which allows for upward speculation because it reduces the shares in circulation), included as part of a total repurchase program of $9 billion over 3 years . Rarely seen in a calendar year .

Cash surplus generated over the financial year: $0.1 billion ($1.8 billion - $1.7 billion which is added to the previous cash flow of 12/31/2018).

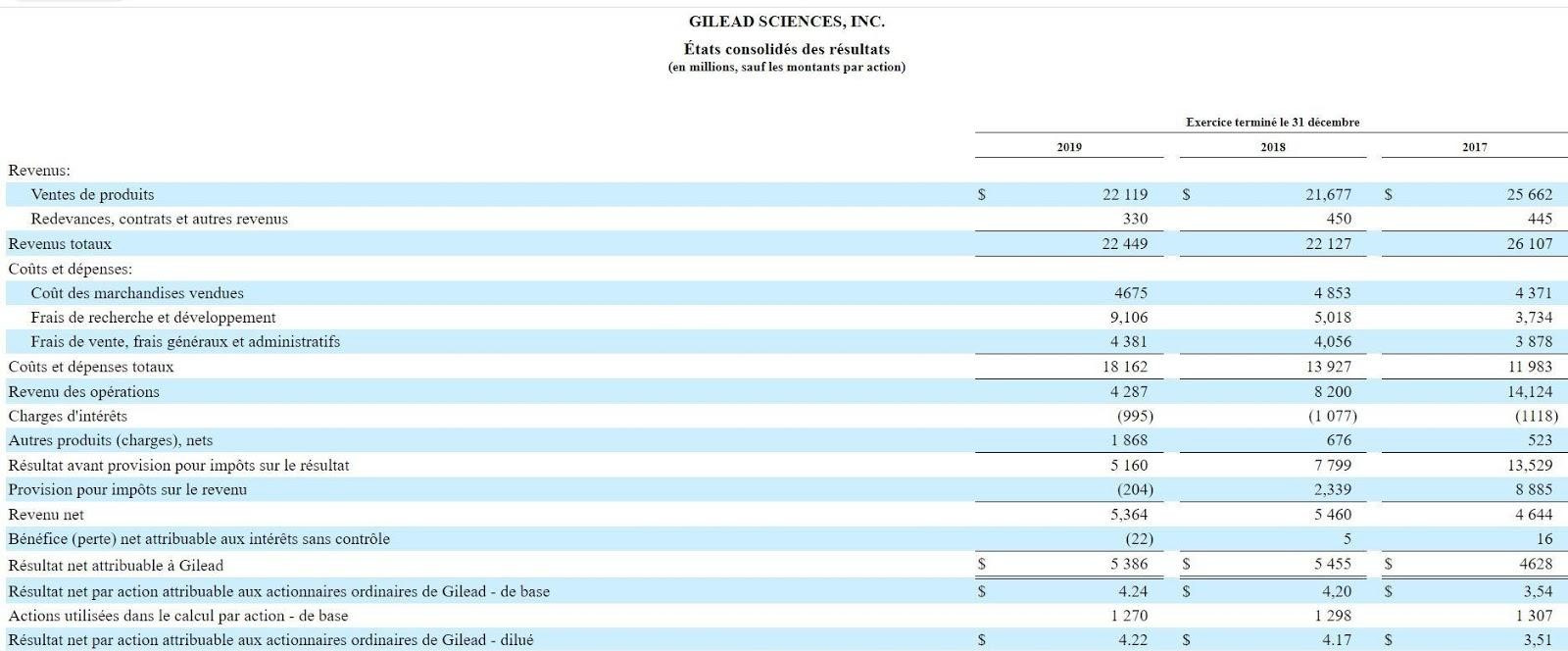

Income statements

A 2019 turnover of $22.4 billion , down compared to 2017 of $26.1 billion. Its evolution must be nuanced because until 2017 Gilead's strategy probably reached certain limits: internal R&D without major discoveries, combined with external growth operations by buying smaller companies and with "best-selling" products. » or “promising” start-ups. With the risk inherent in this strategy of paying too much for a promising start-up, but which has not yet developed anything marketable.

Gilead's external growth strategy therefore boils down to the purchase of start-ups, probably while underestimating the "market" risk, or to the acquisition of companies potentially competing with its flagship products (anti-HIV) to digest them slowly and make them. disappear. We must also take into consideration that economic liberalism across the Atlantic results in anti-monopoly legislation different from that in Europe .

In addition to the external growth strategy, Gilead has opted for a “franchisor” commercial approach by only distributing via “franchised” medical product wholesalers. Which implies an entry fee and a retrocession of turnover on the turnover of its distributors. This strategy ultimately leads to a certain decrease in turnover because at maturity, no distributor is recruited and turnover is concentrated on products at the end of their patent (which therefore become "genericizable").

Gilead still maintains significant leadership in HIV-related products.

It is nevertheless clear that the many fears expressed in writing in the document “2019 Gilead Financial Report” mentioned under the title of this paper are real.

The same causes producing the same effects, too high a concentration of turnover on a single type of product very often leads to serious difficulties in the more or less near future.

What are the results of the $18 billion in cumulative R&D spending that was made in three years?

We can legitimately ask the question in view of the downward trend in turnover, even taking into account the duration of the development of treatments (4/5 years minimum) to achieve a marketable result.

Such a level of investment is reflected in the managerial approach of “finding growth drivers at all costs” . This is reflected in the annexes to the financial report and is far from a completely rational approach given the monstrous weight of these expenses representing 40.56% of turnover for the year 2019 alone. Over 3 years this represents on average 9 .44% of turnover or $2.225 billion per year for $23.561 billion in turnover.

Such a level of investment also often translates into potential managerial concerns about R&D within a group: too often among researchers, some are insufficiently productive and in the absence of a competent manager "above" to detect them, the expenditure staff are flying away.

Interest charges on loans previously raised remain low; the group prefers to finance itself by raising its own funds, part of which is from American pension fund managers such as BlackRock, but without exclusivity.

In addition, the purchase and resale policy of negotiable securities makes it possible to achieve a good part of its final result on these gains (or losses).

In addition there is a policy of repurchasing its own shares on the open market. This can be very important for understanding what is happening globally at the moment in relation to COVID 19.

To illustrate the point, let's take an example: By buying back, for example, 5% of its own shares in circulation on the stock market, only 95% remains in circulation. Various press releases, accompanied by major global lobbying associated with the development of a promising treatment (for example in the fight against Covid) trigger interest in the company. This renewed interest in the company's shares leads to an increase in the value of all shares, the 95% as well as the 5% in treasury shares. Investors are always sensitive to the effects of announcements or analyses, without necessarily verifying the reality, preferring to buy immediately in order to participate in the increase in valuation.

The collateral advantage for the company is to also have a latent capital gain on the securities it owns! It will simply be necessary to gradually reinject them into the market so as not to create oversupply or to sell them over the counter to another group, to generate very significant profits. With the possibility of manipulating investors through regular and excessively optimistic press releases.

With these different points, Gilead generates $5.386 billion in net income, fairly stable but with the extrinsic risks mentioned at the very beginning of the analysis on the weight too concentrated on HIV (78%) and on the absence of reliable discovery and marketable despite the billions invested in R&D.

Balance sheets (summary)

Analysis of balance sheets:

A debt ratio (Gearing: long-term bank debts / Total Equity) which oscillates around 100%, with an overall cash flow making it possible to repay annual capital installments and pay substantial dividends , while causing capital gains on securities held via the program detailed in the appendices to the annual report.

$9 billion in repurchase of Gilead shares by Gilead was decided 3 years ago to at least support the price of the securities and achieve substantial capital gains with the underlying either a major discovery or press releases which can be optimistic about reality (treatment against Covid).

The discrediting of hydroxychloroquine through a study on a very large sample size, published in a prestigious and respected journal, leaves room for doubt.

Un géant en milliards, mais aux pieds d’argile, encore très solide car :

Trop concentré sur une seule pathologie (le VIH) : 78%

D’énormes dépenses de R&D avec peu de projets qui aboutissent depuis 3 ans (on comprend mieux l’intérêt de trouver une solution contre le Covid en tentant de repositionner une molécule existante, qui n’a pas démontrée son efficacité et dont le développement a coûté plusieurs milliards de dollars.

Une politique de rachat de ses propres actions pour faire monter les actions restant sur le marché libre et en revendre le moment venu avec des plus-values conséquentes. Rien d’illégal en soit, mais l’exercice a ses limites, surtout quand c’est plus à force de communiqués annonçant des « résultats prometteurs » qu’en constatant des « résultats réels » que le cours de Bourse flambe.

Aucune information exacte n’est communiquée sur les dépenses de « lobbying » faites, les données disponibles par ailleurs proviennent des seules déclarations de la société au Center for Responsive Politics.

Gilead Sciences, Inc. a été enregistrée au Delaware le 22 juin 1987 un des paradis fiscaux où l’impôt société est quasi nul. Pourtant c’est en Californie que son siège réel se trouve.

Sans parler des potentiels conflits d’intérêts qu’il peut exister avec entre la société et The Lancet ayant beaucoup d’actionnaires en commun, ainsi que l’inclusion du protocole Remdevisir dans Discovery sans aucune étude clinique préalable démontrant de son efficacité. Pour finir l’étude The Lancet tombe à point nommé puisqu’elle est jugée par beaucoup de spécialistes et scientifiques comme ayant comme seul objectif de disqualifier l’hydroxychloroquine. Les docteurs Mehra et Sapai (co-auteurs de l’étude) ont tous deux indépendamment mentionnés “pourquoi continuer avec une molécule (HCQ) qui a montré son effet toxique et une autre qui a montré une lueur d’espoir (le Remdesivir)”.

Une question supplémentaire devra être posée sur le rôle des actionnaires communs entre Gilead et The Lancet. Comment une publication médicale de renom peut-elle garantir l'intégrité de ses publications et l'indépendance éditoriale en ayant des actionnaires communs? Le mal est fait et the Lancet devra sans aucun doute faire face à une investigation sérieuse des gouvernements pour comprendre ce qui s'est passé et le rôle joué par les diverses parties.

Le cours de l’action Gilead fluctue au gré des annonces avec d'étranges coïncidences. Cela entraine des suspicions de manipulations de cours de bourse (Reuters 1er juin 2020)

"If you shut up truth and bury it under the ground, it will but grow, and gather to itself such explosive power that the day it bursts through it will blow up everything in its way." - Émile Zola

CHRONOS by MacKenzie is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

The Wellness Company operative and former WHO advisor to the White House, Paul Elias Alexander published a paper early in 2020 that helped promote its use.

The Wellness Company operative and former WHO advisor to the White House, Paul Elias Alexander published a paper early in 2020 that helped promote its use.

https://www.medrxiv.org/content/10.1101/2020.05.23.20110932v1.full

Remdesivir causes reactivation of Kaposi’s sarcoma-associated herpesvirus (KSHV) and Epstein-Barr virus (EBV), providing clues for Shingles activation

https://geoffpain.substack.com/p/shingles-caused-by-pfizer-jabs-endotoxin